Kenya’s role as a pioneer in the Malaria Vaccine Implementation Programme has already saved lives, with a 13% reduction in child mortality observed in pilot regions. We are now entering a new phase with the rollout of the R21/Matrix-M vaccine, which is more cost-effective at approximately $3 per dose and boasts nearly 75% efficacy . Beyond vaccines, the 2025 approval of “Coartem Baby” marks the first treatment specifically formulated for infants weighing as little as 2kg .

However, the effectiveness of these high-tech “shields” is threatened by systemic disconnects. A fourth dose is required in the second year of life to maintain protection, yet many families face logistical and financial barriers to returning to the clinic . There is a persistent risk that advanced tools are being deployed in facilities plagued by drug stockouts and aging bed nets that have exceeded their three-year lifespan .

The 2024 El Niño rains served as a reminder of how quickly these systemic gaps can be exposed, causing spikes in transmission among children in poverty-stricken areas with poor drainage . While vaccines offer a high public health impact, their success is tied to the strength of the underlying health system. Without consistent investment in routine care and the replacement of old infrastructure, the protection offered by these new tools risks waning just as the parasite’s resistance rises .

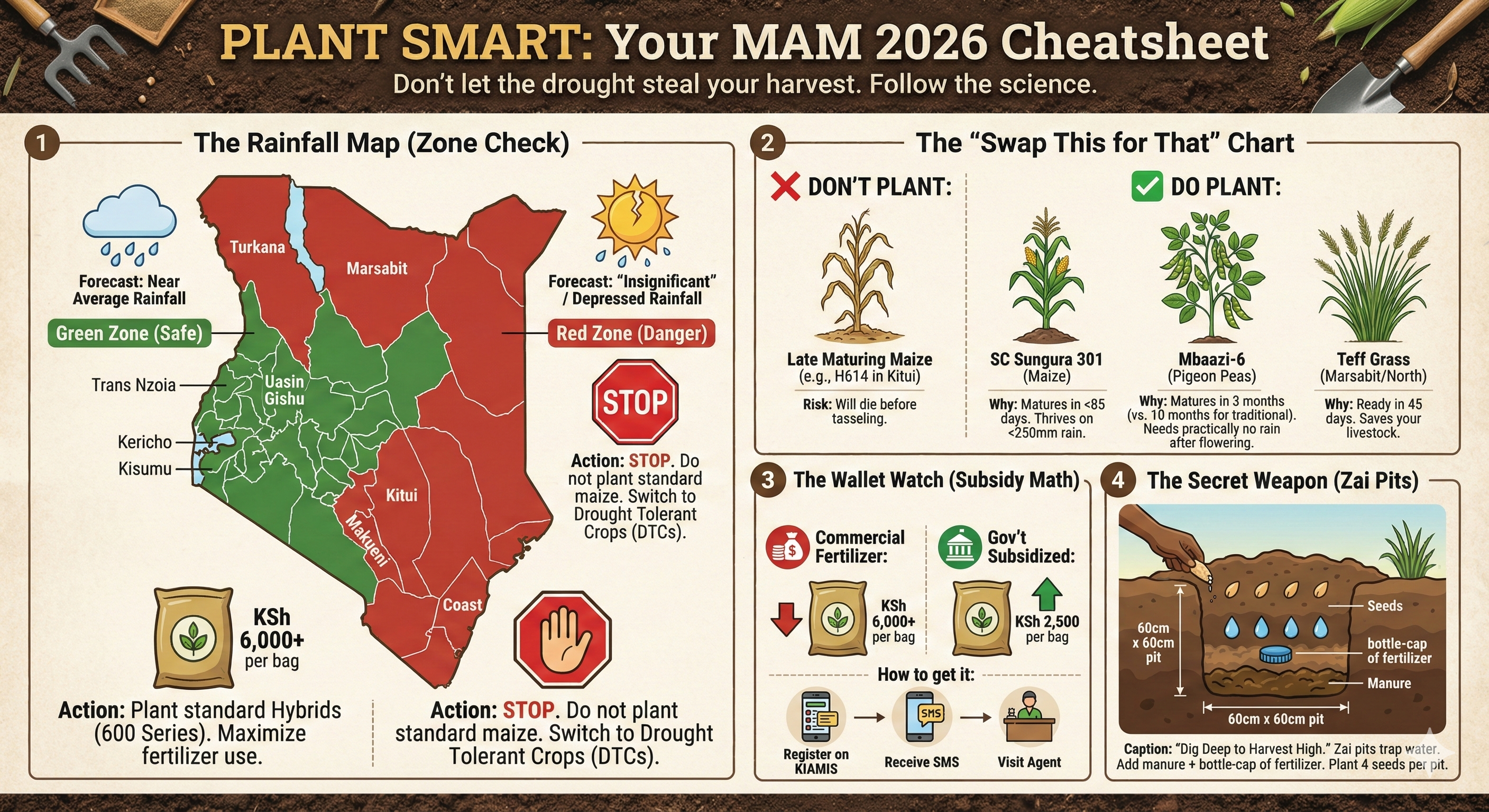

🌱 Stop! Don’t Bury Your Money: The Seeds That Will Survive the 2026 “Insignificant Rains”

Farmers in Arid and Semi-Arid Lands (ASALs) are walking a tightrope. With the Met Department warning of “intermittent dry spells” and poor distribution, planting standard 6-month maize is a gamble you will likely lose.

The “Smart Farm” Swap:

Swap H614 for SC Sungura 301: If you must plant maize, use ultra-early varieties. SC Sungura 301 matures in just 75-85 days and thrives on less than 250mm of rain.

Swap Beans for Mbaazi-6: Traditional pigeon peas take 10 months. The new Mbaazi-6 variety from KALRO is ready in under 3 months. It needs rain only during flowering; after that, it uses deep roots to survive the heat.

Check Dryland Varieties: Look for the DH Series (DH04, DH08) which are specifically bred for these conditions.

References:

Farm Biz Africa Crops that can reach harvest in 2024’s dry short rains

KALRO Climate Smart Agricultural Technologies,Innovations and Management Practices for Green Gram Value Chain

Kenya is watching itself — pixel by pixel. Over the last five years, the country has built an unseen digital nervous system linking thousands of Huawei-powered Safe City cameras, police databases, and social-media monitoring tools. From downtown Nairobi to Mombasa’s seafront, every movement can be captured and cross-checked within seconds at the National Police Service Command Centre. Officials hail this as “smart security”; critics call it the birth of an algorithmic state. It is now evident that Kenya’s system is among the most extensive in sub-Saharan Africa — facial recognition, automatic number-plate readers, and voice analytics feeding a real-time surveillance web. Civil-rights groups such as Article 19 Eastern Africa warn that the same technologies meant to protect citizens are increasingly used to watch them, often without consent or transparency.

The legal architecture meant to contain this power is full of blind spots. The Cybercrimes (Amendment) Act 2024 widened government interception powers and allowed the Communications Authority to pull down online content on loosely defined “security” grounds. Meanwhile, the National Intelligence Service runs data-fusion platforms that combine SIM registration, mobile-money, and tax records — none of which fall under the Data Protection Act’s civilian oversight. The Office of the Data Protection Commissioner cannot audit national-security operations, leaving surveillance programs completely opaque. As the Kenya Human Rights Commission noted in an April 2024 brief, “privacy protections collapse precisely where the State holds the most data.” In the name of safety, a culture of monitoring has replaced a culture of accountability.

Kenya’s experiment is shaping regional norms. The Huawei model first tested in Nairobi has now appeared in Ethiopia, Uganda, and Tanzania, while Western donors — from the EU to Interpol — fund “cyber-capacity” projects that quietly expand the same infrastructure. Analysts describe this as a surveillance compromise: Eastern hardware, Western money, African data. What began as a modernization effort has become a mirror of global power politics — a democracy borrowing the tools of autocracy to stay secure. Unless Parliament enacts a Surveillance Oversight Law and empowers independent audits, Kenya risks institutionalizing fear as policy. The technology that promised protection now records obedience, and in this new digital republic one truth persists: the cameras no longer blink — they remember.

References:

Article 19 Eastern Africa Surveillance, data protection, and freedom of expression in Kenya and Uganda during COVID-19

The Kenyan Wall Street Kenya Upgrades Cybercrime Law to Hand Gov’t Sweeping Powers to Block Websites

The Star Controversial Cybercrime Act: What they said

Huawei Safaricom:Enhancing Security in Kenya with Huawei’s Converged Command & Control Solution

When a private company’s neural nets began to unmask the hidden flows inside M-Pesa, the discovery jolted more than the fintech sector — it forced Kenya to confront a systemic question: who watches the watchers, and on what rules? The rollout of AI-driven compliance tools at Safaricom was never merely a tech upgrade; it arrived as part of a national emergency — a response to international pressure, spiralling fraud, and regulatory failure. The Financial Action Task Force’s increased-monitoring designation and months of global scrutiny had already pushed lawmakers and regulators into a sprint of reforms; industry actors answered with models that could learn patterns humans could not. But those same models required data — vast, granular, and often personal — and the legal scaffolding for such access was changing in real time. Kenya’s recent cyber-law overhaul and parliamentary amendments to the Computer Misuse and Cybercrime Act expanded state powers over online infrastructure, tightened penalties for SIM-swap and phishing offences, and gave the National Computer and Cybercrimes Coordination Committee sweeping directive authority over platforms and applications. Those moves addressed real harms — SIM swap fraud, phishing, and mass laundering — but they also recalibrated the balance between surveillance and rights.

Video Courtesy: The Kenyan Wall Street Youtube Channel

That recalibration is tested in the day-to-day rub of enforcement. Regulators and the ODPC have begun to draw lines: the Data Protection Commissioner’s recent ruling against a major betting operator for excessive data demands underscores the point that AML objectives cannot be a carte blanche for limitless intrusion. In the Betika case the ODPC found the company’s demand for three months of a user’s M-Pesa statements at account-closure to be disproportionate and ordered compensation, signalling that data-minimisation and privacy remain legally enforceable even amid AML pressures. At the same time, FATF’s 2025 monitoring guidance — and independent analysis from ISS Africa — make plain that Kenya must also show measurable results in prosecutions, beneficial-ownership transparency, and risk-based supervision of non-financial entities (including gambling and virtual assets) if it is to repair global confidence. The practical implication is blunt: Kenya cannot satisfy international partners by papering laws alone; enforcement and proportionate procedural safeguards must accompany technical surveillance. Otherwise the country risks swapping one reputational problem (grey-listing) for another — a domestic legitimacy crisis born of heavy-handed data practices.

So where does Kenya go from here? The answer lies in design choices — legal, technical, and institutional — that make accountability a feature, not an afterthought. We recommend three urgent, interlocking reforms that turn the AI question into a governance opportunity: (1) Purpose-bound, time-limited data access. AML or security queries should be scoped narrowly and logged; full transaction histories must not be a default feed into private models. (2) Explainability + redress. Any automated decision that materially affects a person (account freezes, cash-outs blocked, KYC escalations) must carry a succinct, non-technical rationale and a fast appeals channel routed through an independent body. (3) Joint independent oversight. Operationalize a statutory ODPC–FRC technical review board with public reporting obligations, the power to audit both models and data requests, and a mandate to publish redaction and retention metrics. These are not frictionless reforms — they will slow some processes and impose costs — but that trade-off is precisely the point: legitimacy costs less than lost trust. If Kenya stitches these protections into law and practice — and couples them with meaningful prosecution of financial crimes and improved beneficial-ownership registers — it can convert the awkward moment of global scrutiny into a first-mover advantage: an African model of rights-based, explainable AI governance for financial systems. The choices made now will decide whether Kenya’s algorithms become instruments of accountability or mechanisms that hollow out public trust.

References:

Business Daily Security or surveillance? How amended cyber law could reshape Kenya’s online space

Daily Nation How AI can close trust gaps in Africa’s financial systems

The Kenyan Wall Street How Safaricom is Leveraging AI to Bolster M-Pesa Security and Efficiency

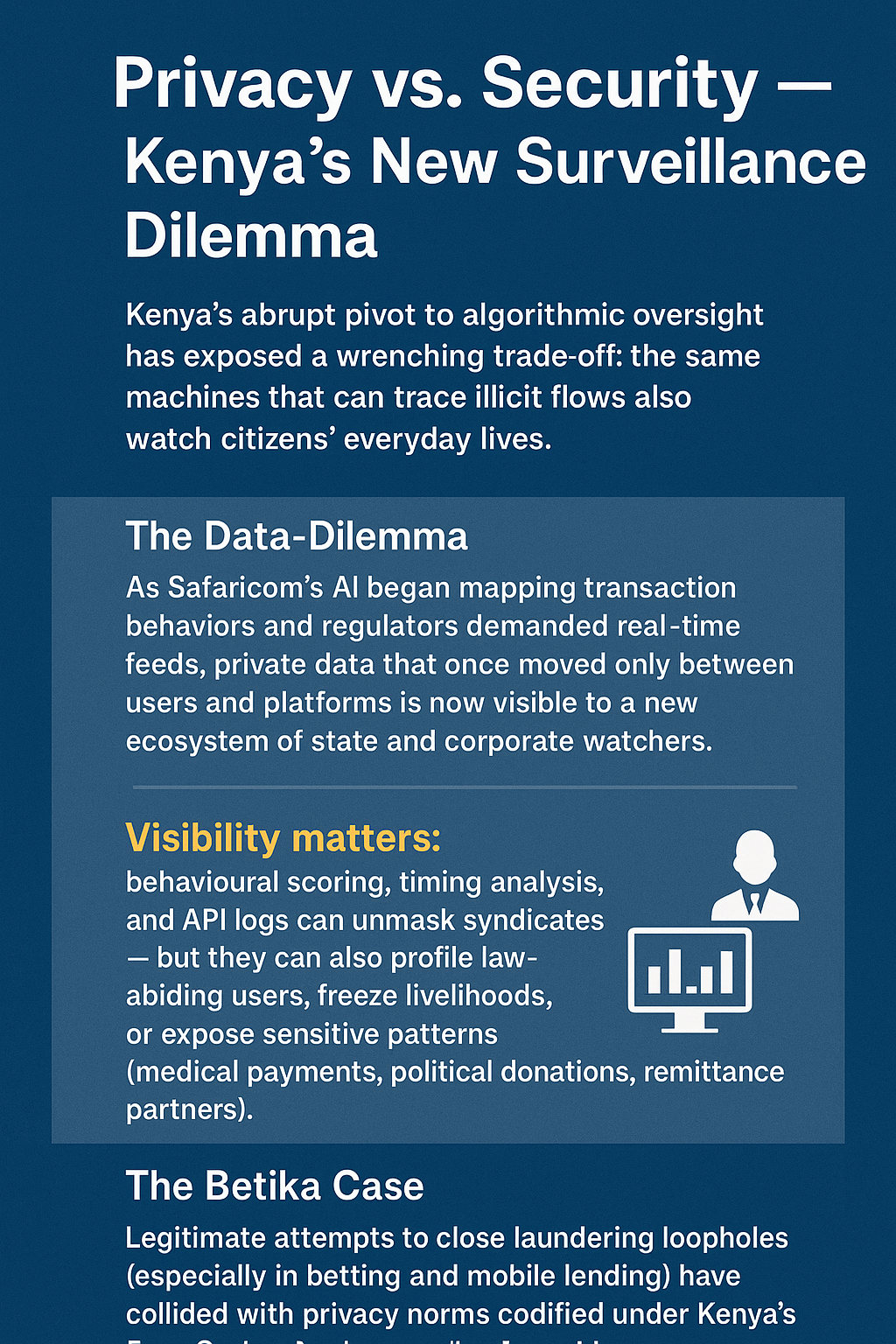

Kenya’s abrupt pivot to algorithmic oversight has exposed a wrenching trade-off: the same machines that can trace illicit flows also watch citizens’ everyday lives. As Safaricom’s AI began mapping transaction behaviors and regulators demanded real-time feeds, private data that once moved only between users and platforms is now visible to a new ecosystem of state and corporate watchers. That visibility matters: behavioural scoring, timing analysis, and API logs can unmask syndicates — but they can also profile law-abiding users, freeze livelihoods, or expose sensitive patterns (medical payments, political donations, remittance partners). In practice, this tension has a name and a face: legitimate attempts to close laundering loopholes (especially in betting and mobile lending) have collided with privacy norms codified under Kenya’s Data Protection laws and enforced by the Data Protection Commissioner. The friction is no longer theoretical — it plays out in court rulings and public grievances, where an automated alert can instantly strand a small-business owner awaiting payroll, or a migrant worker trying to send school fees home.

One high-profile example is the case involving Betika, which was ordered to pay KSh 250,000 for breaching data privacy rules. The ruling found that Betika had improperly processed users’ personal data without sufficient protections or lawful grounds. This case highlights a critical danger: when betting platforms (already under AML scrutiny) become nodes of state data demand, weak privacy compliance means corporate actors — not just regulators — can overreach data collection and usage, compounding surveillance risk. The Betika ruling proved that courts are willing to hold fintech operators accountable, but the scale of risk grows when those same APIs feed into AI-driven compliance systems without clear limits or safeguards.

The policy question is therefore blunt: how do you operationalize intrusive yet effective AML tools without creating a surveillance grid that punishes innocents? The answer requires more than slogans. It begins with strict, purpose-limited access: authorities and private partners should get only the minimal data needed to investigate a flagged flow — not full transaction histories. It requires explainable AI, where users receive understandable notices about why their wallet was flagged, and a clear appeals process exists. It demands robust oversight: the ODPC and FRC must enforce audit protocols, redress mechanisms, and limits on data retention and use. The Betika precedent is a warning: tightening oversight without privacy guardrails risks turning compliance into exclusion and exposing digital citizens to data abuse. Kenya now stands at a critical juncture: Will it build a system where enforcement respects rights — or drift into a regime where surveillance becomes default, and trust becomes collateral damage? In our next post, we’ll explore how to build explainable AI and regulatory harmony — practical steps to reconcile compliance, innovation, and rights.

References:

iGamingToday Betika ordered to pay KSh 250,000 for breaching data privacy rules

Subex How AI and Analytics Are Revolutionizing Fraud Detection in Mobile Money

Thomson Reuters AML challenges in evolving threat landscape, says ACAMS report

Techcabal How Safaricom’s AI exposed money laundering in Kenya’s betting boom

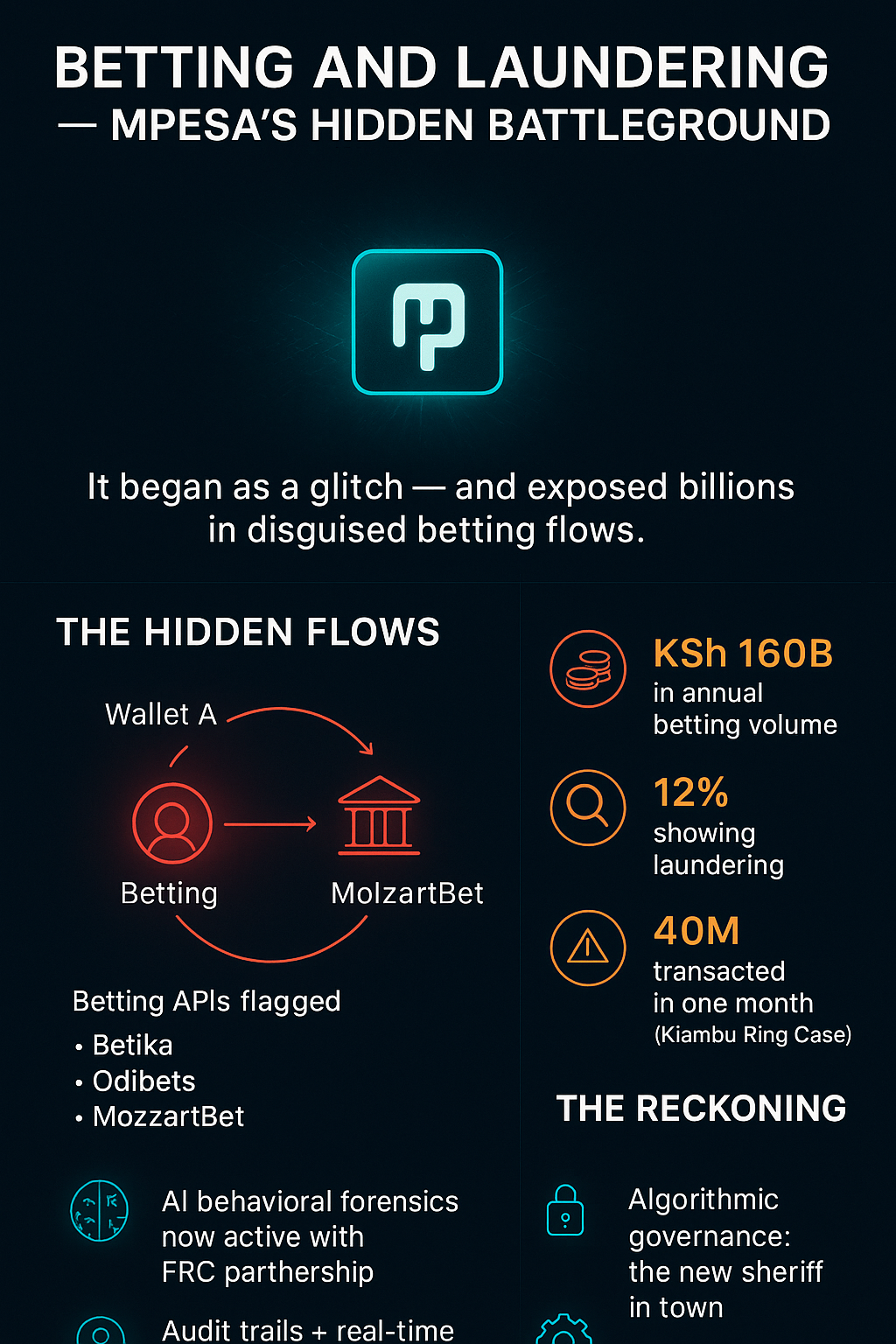

It began as a flicker of digital noise deep within Safaricom’s new artificial intelligence compliance system — a pattern so strange, even the engineers thought it was a software glitch. Betting wallets were trading in micro-loops, small deposits bouncing across networks at impossible speed, masquerading as gaming wins. But when the algorithm slowed the data stream, it exposed the truth: this wasn’t gambling; it was laundering. In days, Safaricom’s AI had flagged dozens of high-traffic betting APIs — among them Betika, Odibets, and MozzartBet — for suspicious activity, their systems pulsing with repeated micro-transactions that defied legitimate gaming behavior. What the model revealed was staggering. Ordinary player wallets had become conduits for billions of shillings, circulating under the guise of lucky streaks. Behind every spin, every small bet, was a meticulously choreographed web of digital cash-washing. The machine had finally confirmed what regulators long suspected but could not prove: Kenya’s fast-rising betting culture had evolved into the perfect laundromat — one hidden in plain sight inside the M-Pesa ecosystem.

The numbers told their own story. In the Kiambu Betting Ring case, investigators uncovered agents processing over KSh 40 million in just one month, using layered deposits and false payout slips to disguise dirty money as betting gains. Similar patterns appeared in the MozzartBet compliance freeze of mid-2024, where offshore cash-outs linked to unverified wallet owners triggered intervention by the Financial Reporting Centre (FRC) and Central Bank’s AML unit. By then, the data was irrefutable. AI modeling suggested that nearly 12 percent of Kenya’s annual betting volume — roughly KSh 160 billion — showed characteristics of laundering or structured fraud. The algorithms traced wallet behaviors that no manual audit could — bettors who “won” every day without ever placing bets, agents whose transaction volumes exceeded physical limits, and accounts that went dark after a single large payout. These were not random outliers; they were engineered identities, designed to game a system built for speed, not scrutiny. For years, M-Pesa’s success story — its promise of instant, borderless convenience — had inadvertently created the perfect storm: a seamless digital infrastructure exploited by syndicates more agile than the law itself.

Now, that same infrastructure is being weaponized against them. Safaricom’s AI partnership with the FRC has ushered in a new era of behavioral forensics — algorithms that don’t just track money but interpret motion, timing, and correlation. Yet this technological awakening has sparked backlash. Betting firms accuse Safaricom of overreach, freezing legitimate transactions and blurring the line between compliance and surveillance. Regulators, meanwhile, are tightening the screws: audit trails for all gaming wallets, mandatory KYC verification, and real-time data access for AML enforcement. The ripple effects extend far beyond gaming. Kenya’s digital economy now stands at an inflection point, where algorithmic oversight has become both protector and disruptor. In exposing how entertainment masked economic deceit, the AI has done more than flag fraudulent wallets — it has held up a mirror to the fragility of digital trust in a cashless nation. The house may always win, but in this new frontier, so does the machine — and its vision is only getting sharper.

References:

Techcabal Safaricom fires 113 employees over fraud as internal cases rise

KBC Channel 1 Kenya’s gambling industry set for shake-up after President Ruto signs into law Gambling Control Bill (Youtube)

The Kenyan Wall Street How Safaricom is Leveraging AI to Bolster M-Pesa Security and Efficiency

KBC M-pesa outage on Monday as Safaricom adopts AI to tame fraud

In March 2025, we examined the rising concerns over Kenya’s Competency-Based Curriculum (CBC) rollout, where critics warned that critical academic foundations were being neglected in the rush toward specialization as discussed here. Chief among these concerns was the controversial proposal to make mathematics optional for students in the Arts & Sports Science and Social Sciences pathways at the senior secondary school level. Many stakeholders — including professional bodies, educators, and parent associations — argued that removing compulsory mathematics risked undermining students’ critical thinking, problem-solving ability, and future career flexibility. The fears were compounded by Kenya’s broader ambitions to remain competitive in a global economy increasingly shaped by STEM skills and data-driven professions. As the CBC pathways were being finalized for the Grade 10 transition starting in 2026, it became clear that significant gaps remained between the curriculum’s vision and its practical implications. It is against this backdrop that, in April 2025, the Ministry of Education announced a major policy reversal: mathematics would once again be mandatory across all senior secondary school pathways, not just for STEM students. This reinstatement signals an important shift toward reinforcing core competencies while still pursuing specialization — a recognition that a solid academic base is essential for building adaptable, future-ready graduates.

A Report by KTN News Kenya

The decision to reverse course on mathematics came after intense, organized advocacy by various stakeholder groups who viewed the optionalization of math as a dangerous policy misstep. Organizations such as the Institution of Engineers of Kenya (IEK), the Kenya Union of Post-Primary Education Teachers (KUPPET), and the Architectural Association of Kenya (AAK) were among the most vocal opponents. They collectively warned that sidelining mathematics would erode essential competencies needed across all fields, not just technical ones. Their arguments framed mathematics as the “language” underpinning modern engineering, architecture, finance, digital technology, and even the creative industries — emphasizing that basic numeracy is now a universal life skill, not a niche technical ability. During the national dialogues on CBC reforms, a strong consensus emerged that foundational subjects like mathematics cannot be optional in a 21st-century education system. CS Julius Ogamba acknowledged the impact of this feedback during the announcement, positioning the Ministry’s U-turn as evidence of a responsive government willing to adjust policy based on real-world insights. However, this shift, while welcome, also highlights earlier weaknesses in CBC policy design — suggesting that insufficient consultation with key professional sectors had left the initial plans vulnerable to critical gaps. It also underlines a broader tension within the CBC framework: the challenge of balancing meaningful specialization with maintaining a strong, common academic foundation across diverse student pathways.

To operationalize the reinstated mathematics requirement, the Ministry of Education — in collaboration with the Kenya Institute of Curriculum Development (KICD) — has adopted a differentiated model. Students following the STEM pathway will study “pure mathematics,” covering advanced concepts necessary for science and technology careers. Meanwhile, those pursuing Arts & Sports Science and Social Sciences will engage with a “simplified” or “foundational” version of mathematics aimed at building essential problem-solving and numeracy skills relevant to their fields. While this solution addresses stakeholder demands for universal mathematical literacy, it simultaneously introduces a new layer of complexity into an already strained CBC implementation process. The development of two distinct mathematics curricula will require extensive work by KICD to ensure each pathway remains rigorous and coherent. Additionally, the Teachers Service Commission (TSC) must ensure that sufficient numbers of teachers are trained and deployed to deliver differentiated mathematics instruction effectively — a tall order given existing shortages and capacity constraints highlighted in previous CBC evaluations. Schools will also need updated materials, tailored assessments from KNEC, and sufficient infrastructure to handle new teaching demands. In short, while reinstating compulsory mathematics is a vital corrective step, it magnifies the resource, training, and logistical challenges already dogging CBC’s transition. It also reinforces a broader lesson for education reform: that protecting foundational skills must remain central, even as systems innovate and specialize for a changing world.

References:

All Africa Kenya: Mathematics to Remain Compulsory in Primary and Secondary Schools

The Eastleigh Voice State makes Math mandatory for all CBC senior school learners after public outcry

The Standard Maths no longer compulsory as CBC pioneers set to pick careers

The Standard Stakeholders raise concerns over Math specialisation at Senior Schools

Capital News Mathematics to remain compulsory in primary and Secondary Schools

Jijuze Concerns Over Kenya’s Competency-Based Curriculum Implementation

The inaugural Global AI Summit for Africa in Kigali marked a pivotal moment, underscoring the continent’s ambition to become a significant player in the global artificial intelligence landscape. The summit, themed around leveraging AI for Africa’s demographic dividend, brought together leaders to discuss the immense potential of AI to drive economic growth and enhance social welfare across various sectors. From revolutionizing healthcare through AI-powered diagnostics and telemedicine to transforming education with personalized learning and breaking down language barriers, the opportunities for Africa to leapfrog traditional development stages are substantial. In agriculture, AI promises to optimize crop yields and improve resource management, while in governance, it offers tools for greater efficiency and transparency. This enthusiasm is tempered by the recognition of significant hurdles that need to be addressed for this potential to be fully realized.

A Report by France 24

Despite the bright prospects, the widespread adoption of AI in Africa faces considerable challenges. These include significant infrastructure deficits in computing power and internet connectivity, the complexity of linguistic diversity hindering the development of inclusive AI models, and limitations in the availability of high-quality, relevant data. Furthermore, a notable skills gap in AI-related fields and the imperative to establish ethical and regulatory frameworks are critical considerations. However, African innovation is already emerging to tackle these challenges. For instance, BuniAI is making strides in enhancing digital accessibility by simplifying the creation of USSD applications. This technology is particularly relevant in Africa, where basic mobile phones are prevalent, offering a crucial pathway to bridge the digital divide and deliver essential services and information to underserved populations.

The path forward for AI in Africa requires a concerted effort from governments, investors, educational institutions, and the private sector. Strategic investments in infrastructure, talent development, and the cultivation of local innovation ecosystems are crucial. Moreover, fostering strong public-private partnerships and promoting ethical AI development that is tailored to Africa’s unique context and values will be essential to ensure that the benefits of AI are inclusive and sustainable. The discussions and commitments made at the Kigali summit, coupled with the work of innovative organizations like BuniAI, signal a determined move towards harnessing the transformative power of artificial intelligence to shape a more prosperous and equitable future for the African continent.

References:

The East African Why Africa has a real chance to lead the way in AI

Malawi Ace Artificial Intelligence: Africa’s Opportunity to Leapfrog Development

African Business Global AI Summit on Africa: Can policymakers take control of AI?

Nairobi is set to revolutionize its traffic management with a Sh7.9 billion investment in an intelligent traffic system (ITS) financed by the Economic Development Cooperation Fund via the Export-Import Bank of Korea. The project will deploy AI-driven technology across 125 intersections—starting with 25 major junctions scheduled for completion by February 2027—in an effort to modernize urban mobility and reduce severe congestion, which currently drains an estimated Sh120 billion from the economy annually. With Kenya’s GDP (PPP) reaching USD 375.36 billion in 2024 and East Africa projected to post 6% regional growth in 2025, this initiative represents a critical step in transforming urban infrastructure. While focusing primarily on general traffic flow management, Nairobi’s plan hints at future phases that could integrate public transport, aligning its long-term vision with regional developments in cities like Addis Ababa and Dar es Salaam, where specialized systems already target bus rapid transit and multimodal transportation networks.

A Report about AI-Powered Smart Traffic Control System by See The Nature

A comparative look at regional systems reveals key differences and opportunities for Nairobi’s ITS. Unlike Dar es Salaam’s ITS, which prioritizes the safety, mobility, and efficiency of its Bus Rapid Transit (BRT) network through real-time data integration for operators and passengers, Nairobi’s initial emphasis remains on managing overall traffic flow. However, adopting elements from Tanzania’s broader national-level ITS strategy could guide future expansions to incorporate public transit more effectively. International best practices underscore Nairobi’s strengths, such as the use of artificial intelligence for real-time traffic control and automated violation detection—tools that could enhance enforcement and reduce the reliance on manual policing. Yet, critical areas need further detailing: adherence to open standards like NTCIP for system interoperability, designing a scalable architecture to support future technological advancements, and outlining clear protocols for data handling and compliance with Kenya’s Data Protection Act 2019. Moreover, the success of this system will hinge on robust internet connectivity (currently at 79%), a reliable fiber optic infrastructure, and comprehensive legal frameworks to govern data security and system operations.

A Report by CGTN Africa

For Nairobi’s ITS to achieve its full potential, a strategic approach incorporating both technical and community-focused recommendations is essential. Authorities should invest heavily in a resilient technological infrastructure—upgrading internet and sensor networks, expanding data processing capabilities, and resolving fiber optic disputes—to ensure that the system can handle the massive data volumes generated. Equally important is the establishment of a strong legal and regulatory framework that not only complies with Kenya’s Data Protection Act but also aligns with national traffic management policies and international standards. Public awareness and training initiatives are crucial; educating citizens on system benefits and new traffic protocols, while training traffic engineers and law enforcement on system management, will foster community acceptance and smooth implementation. In addition, measures to mitigate risks such as power outages, vandalism, and cybersecurity breaches must be integral to the project’s design. By embracing international best practices, encouraging collaboration with cities that have successfully implemented ITS, and focusing on scalability and reliability, Nairobi is poised not only to alleviate congestion but also to emerge as a regional leader in intelligent transportation, paving the way for a smarter, safer, and more sustainable urban future.

References:

The Star Samsung to build Nairobi’s Sh7.9bn intelligent traffic system

Kenyans.co.ke KURA to Begin Construction of AI-Powered Smart Traffic System in Nairobi This April

Kenya’s financial technology sector has emerged as a dominant force in the nation’s economy, fueled by a remarkable surge in corporate investment aimed at fostering innovation and supporting the growth of Micro, Small, and Medium Enterprises (MSMEs). This thriving ecosystem is built upon the bedrock of widespread mobile money adoption, with Kenya boasting one of the highest penetration rates globally, making digital financial transactions a common practice for a vast majority of the population. Recognizing this fertile ground, the corporate sector has stepped in as a crucial catalyst, injecting substantial capital into fintech startups through various avenues, including direct equity investments, the establishment and backing of incubation and acceleration programs, and the formation of strategic alliances. These concerted efforts have not only driven significant investment inflows but have also empowered fintech companies to develop and scale cutting-edge solutions specifically designed to address the unique needs of MSMEs, which form the backbone of the Kenyan economy by employing over 80% of the workforce.

A Report by KTN News Kenya

The impact of this corporate-driven investment in fintech is being felt profoundly by MSMEs across Kenya, primarily through enhanced access to vital financial services that were previously out of reach for many. Fintech innovations, often nurtured and funded by corporate initiatives, are providing working capital solutions, facilitating the adoption of digital payment systems, and offering essential business management tools. Leading corporations such as Safaricom, through its Spark Venture Fund and collaborations like the Spark Accelerator, alongside M-Pesa Africa’s partnerships with Microsoft for digital skills training and Mastercard for expanding digital payment infrastructure, are at the forefront of this transformation. The Co-operative Bank of Kenya’s collaboration with the International Finance Corporation (IFC) to launch tailored financial solutions for MSMEs further underscores the commitment of established financial institutions to this sector. These strategic partnerships and investments are enabling small businesses to overcome traditional barriers to growth, streamline their operations, and tap into broader markets, ultimately contributing to job creation and economic prosperity.

Despite the remarkable progress, the journey of corporate investment in Kenyan fintech and its support for MSMEs is not without its hurdles. Challenges such as navigating the evolving regulatory landscape, managing increasing competition within the fintech space, securing sufficient capital for scaling, and mitigating the ever-present threat of cybersecurity remain significant considerations. However, the opportunities that lie ahead are equally compelling, with fintech possessing the inherent ability to achieve greater reach in underserved areas, foster continuous innovation in financial service delivery, and significantly enhance financial inclusion for individuals and businesses alike. The continued collaboration between corporations and agile fintech startups, exemplified by successful partnerships that are already delivering tangible benefits to MSMEs, signals a promising future for the sector, paving the way for sustained growth, further technological advancements, and a more financially empowered and inclusive Kenyan economy.

References:

The Star Fintech, digital content startups compete for investor backing

FinTech Africa Fintech Emerges as Kenya’s Most Prevalent Tech Startup Sub-Sector