The final frontier of the malaria fight is as much about economics and topography as it is about biology. As temperatures rise, malaria is climbing into highland areas where populations lack natural immunity . Research shows that “U-shaped” valleys in these regions are five times more likely to host parasites than steeper “V-shaped” valleys, as their flat floors provide stagnant water for vector breeding.

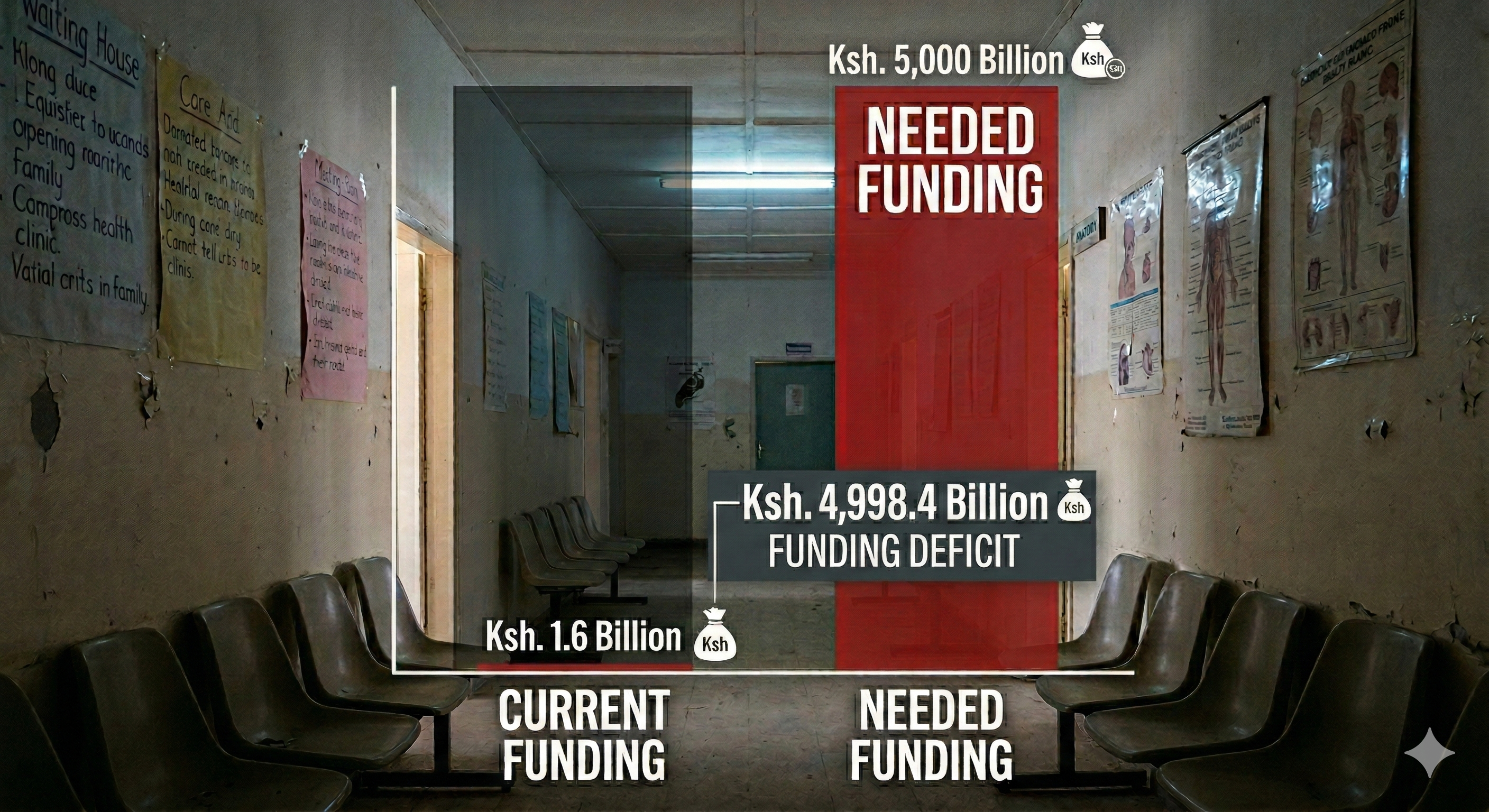

While Kenya’s 2023-2027 strategy aims for a 90% reduction in deaths, these goals are currently balanced on the edge of a financial abyss . In 2024, global malaria funding reached only $3.9 billion—less than half of what is needed annually. Abrupt 2025 US funding cuts have triggered a “cascading collapse” in health infrastructure, with nearly 25,000 community health workers in Kenya facing imminent layoffs .

Without sustainable, government-led financing models, the health system remains vulnerable to unplanned disruptions. To secure a malaria-free future, Kenya must pivot toward local manufacturing of diagnostics and vaccines while integrating climate data into every level of health governance. The line between a breathtaking view of elimination and a dangerous resurgence is currently dependent on filling these “ghost deficits” in aid.

References:

Human Rights Watch Donor Nation Cuts to Global Health Financing Affect Millions

Physicians for Human Rights “The System is Folding in on Itself”: The Impact of U.S. Global Health Funding Cuts in Kenya

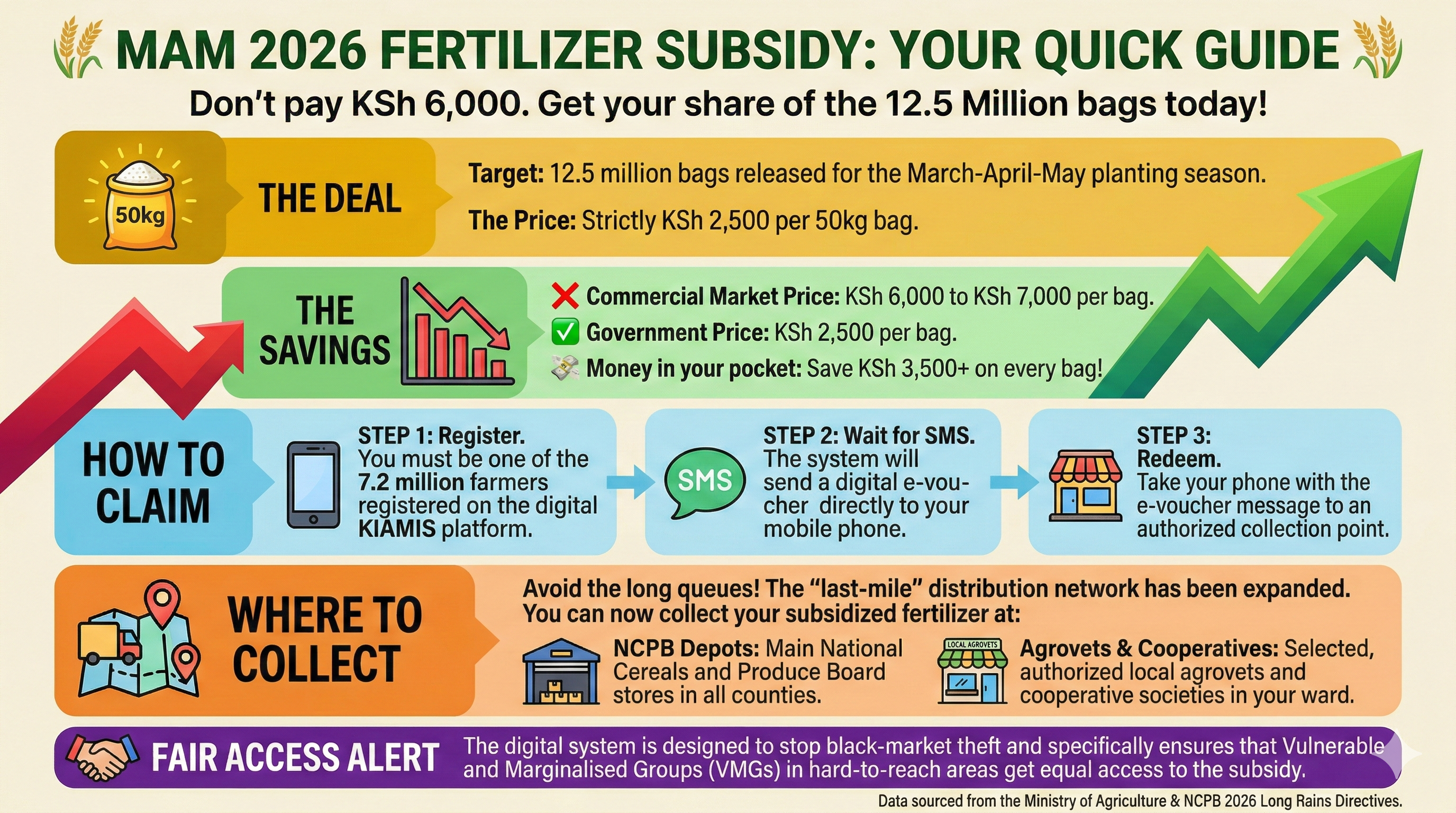

💰 KSh 2,500 Fertilizer: How to Bypass the Queues and Get Your Share

The government has released 12.5 million bags of subsidized fertilizer for the 2026 Long Rains, capping the price at KSh 2,500 per bag (down from market rates of KSh 6,000+).

The Catch? You Must Be Digital. Gone are the days of just showing up at the NCPB.

Register: Ensure you are listed on the KIAMIS (Kenya Integrated Agricultural Management Information System) platform.

Wait for the SMS: You will receive an e-voucher on your phone.

Collect: Go to your nearest NCPB depot or registered agro-vet agent.

References:

Streamline Operation Long Rains: State Floods Market with 12.5 Million Bags of Subsidized Fertilizer

Ratin Agriculture Ministry Flags Off Major Fertiliser Distribution to Strengthen Food Security

Kenya’s role as a pioneer in the Malaria Vaccine Implementation Programme has already saved lives, with a 13% reduction in child mortality observed in pilot regions. We are now entering a new phase with the rollout of the R21/Matrix-M vaccine, which is more cost-effective at approximately $3 per dose and boasts nearly 75% efficacy . Beyond vaccines, the 2025 approval of “Coartem Baby” marks the first treatment specifically formulated for infants weighing as little as 2kg .

However, the effectiveness of these high-tech “shields” is threatened by systemic disconnects. A fourth dose is required in the second year of life to maintain protection, yet many families face logistical and financial barriers to returning to the clinic . There is a persistent risk that advanced tools are being deployed in facilities plagued by drug stockouts and aging bed nets that have exceeded their three-year lifespan .

The 2024 El Niño rains served as a reminder of how quickly these systemic gaps can be exposed, causing spikes in transmission among children in poverty-stricken areas with poor drainage . While vaccines offer a high public health impact, their success is tied to the strength of the underlying health system. Without consistent investment in routine care and the replacement of old infrastructure, the protection offered by these new tools risks waning just as the parasite’s resistance rises .

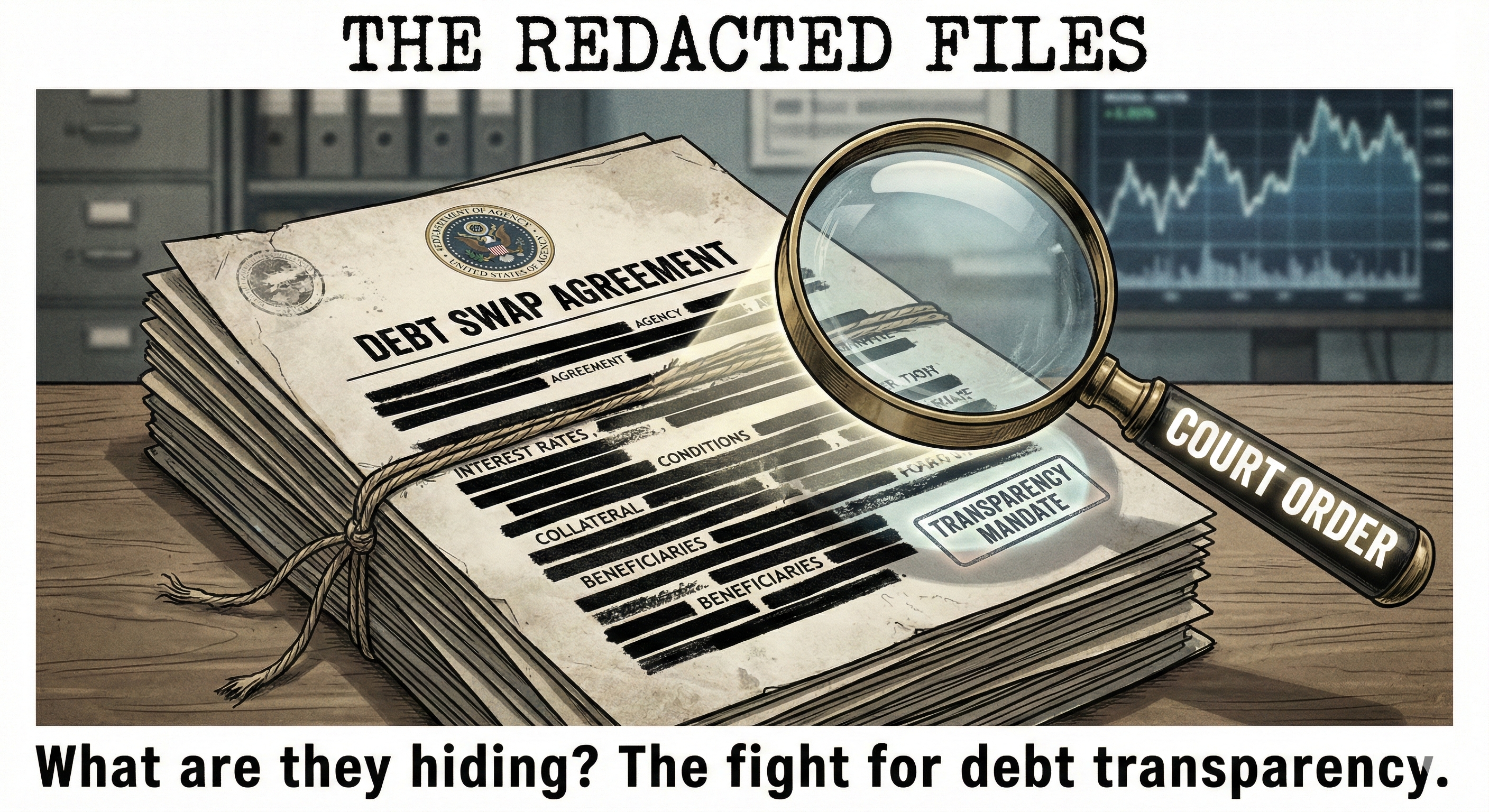

Despite the high stakes, the specific terms of the debt-for-food swap remain shrouded in secrecy, sparking legal battles and civil society alarm. A case filed at the East African Court of Justice, Wanjiru Gikonyo v The Attorney General, challenges the government’s refusal to disclose the full details of sovereign debt agreements. Litigants argue that committing future tax revenues and “savings” to long-term projects without public participation is unconstitutional. The lack of a public dashboard detailing exactly how the Sh129 billion will be spent creates a “transparency deficit” that invites mismanagement.

This opacity exacerbates the “sovereignty paradox.” By allowing the US-DFC and WFP to dictate the terms of expenditure, Kenya is effectively admitting that its own institutions cannot be trusted. While external conditionality acts as a safeguard against local corruption, the public remains in the dark about what exactly has been signed away. Are there hidden fees? What are the penalties for non-compliance? Without full disclosure, the Kenyan taxpayer is a passenger in a vehicle being driven by foreign creditors.

Transparency is not just a legal formality; it is the only disinfectant strong enough to prevent the “bureaucratic consignment” of funds. Civil society is demanding that the Treasury publish every shilling of the “savings” and every project beneficiary. Until then, the debt swap remains a “black box”—a deal negotiated in boardrooms in Washington and Nairobi, with the bill sent to the citizen who has no say in the menu.

References:

Afronomics Law Sovereign Debt News Update No. 147: The Promises and Transparency Pitfalls of Kenya’s $1 Billion Debt-for-Food Swap

The Institute for Social Accountability The High Court has ordered the National Treasury to disclose critical information on Kenya’s bilateral loans and sovereign bonds.

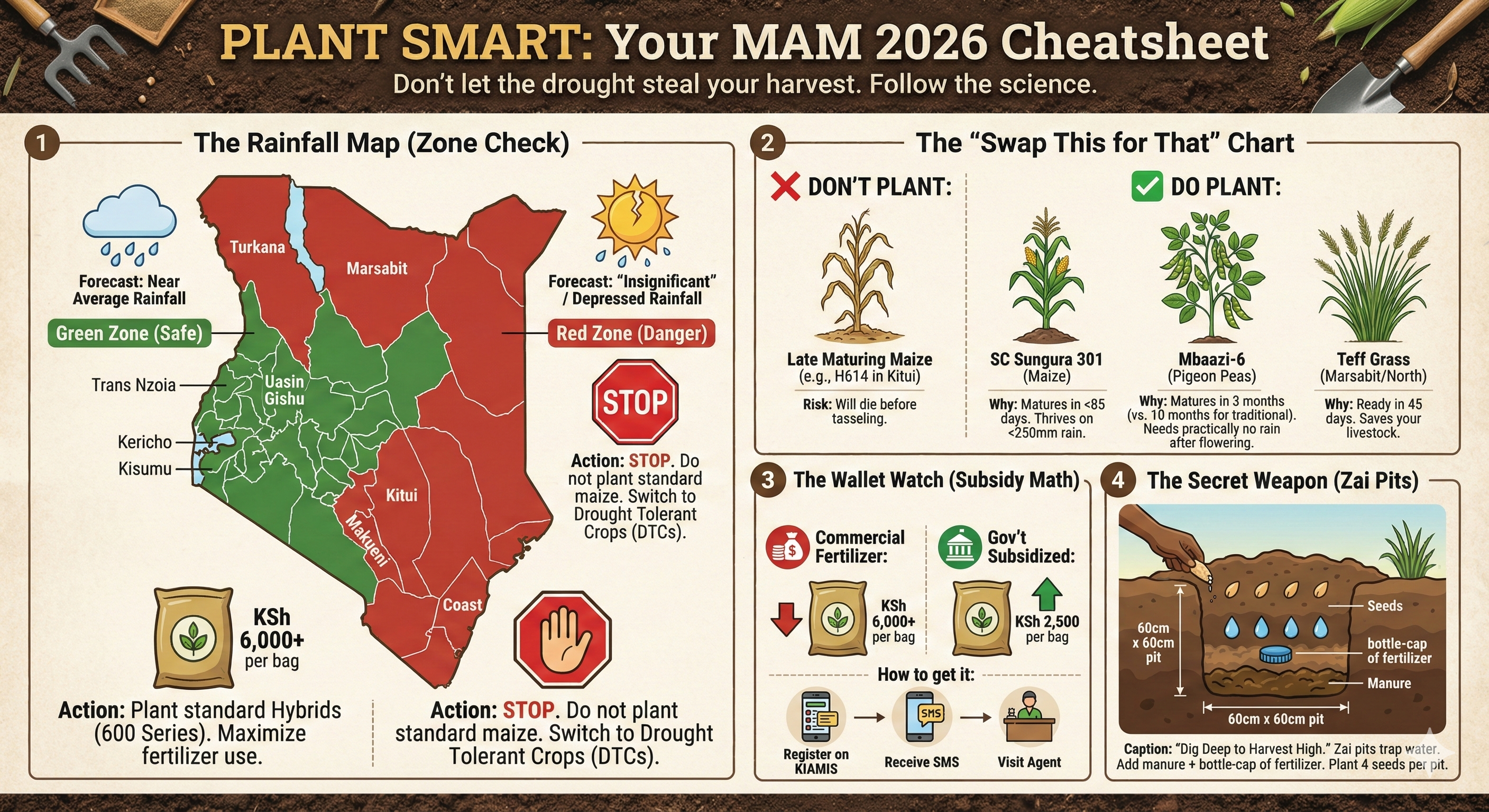

🌱 Stop! Don’t Bury Your Money: The Seeds That Will Survive the 2026 “Insignificant Rains”

Farmers in Arid and Semi-Arid Lands (ASALs) are walking a tightrope. With the Met Department warning of “intermittent dry spells” and poor distribution, planting standard 6-month maize is a gamble you will likely lose.

The “Smart Farm” Swap:

Swap H614 for SC Sungura 301: If you must plant maize, use ultra-early varieties. SC Sungura 301 matures in just 75-85 days and thrives on less than 250mm of rain.

Swap Beans for Mbaazi-6: Traditional pigeon peas take 10 months. The new Mbaazi-6 variety from KALRO is ready in under 3 months. It needs rain only during flowering; after that, it uses deep roots to survive the heat.

Check Dryland Varieties: Look for the DH Series (DH04, DH08) which are specifically bred for these conditions.

References:

Farm Biz Africa Crops that can reach harvest in 2024’s dry short rains

KALRO Climate Smart Agricultural Technologies,Innovations and Management Practices for Green Gram Value Chain

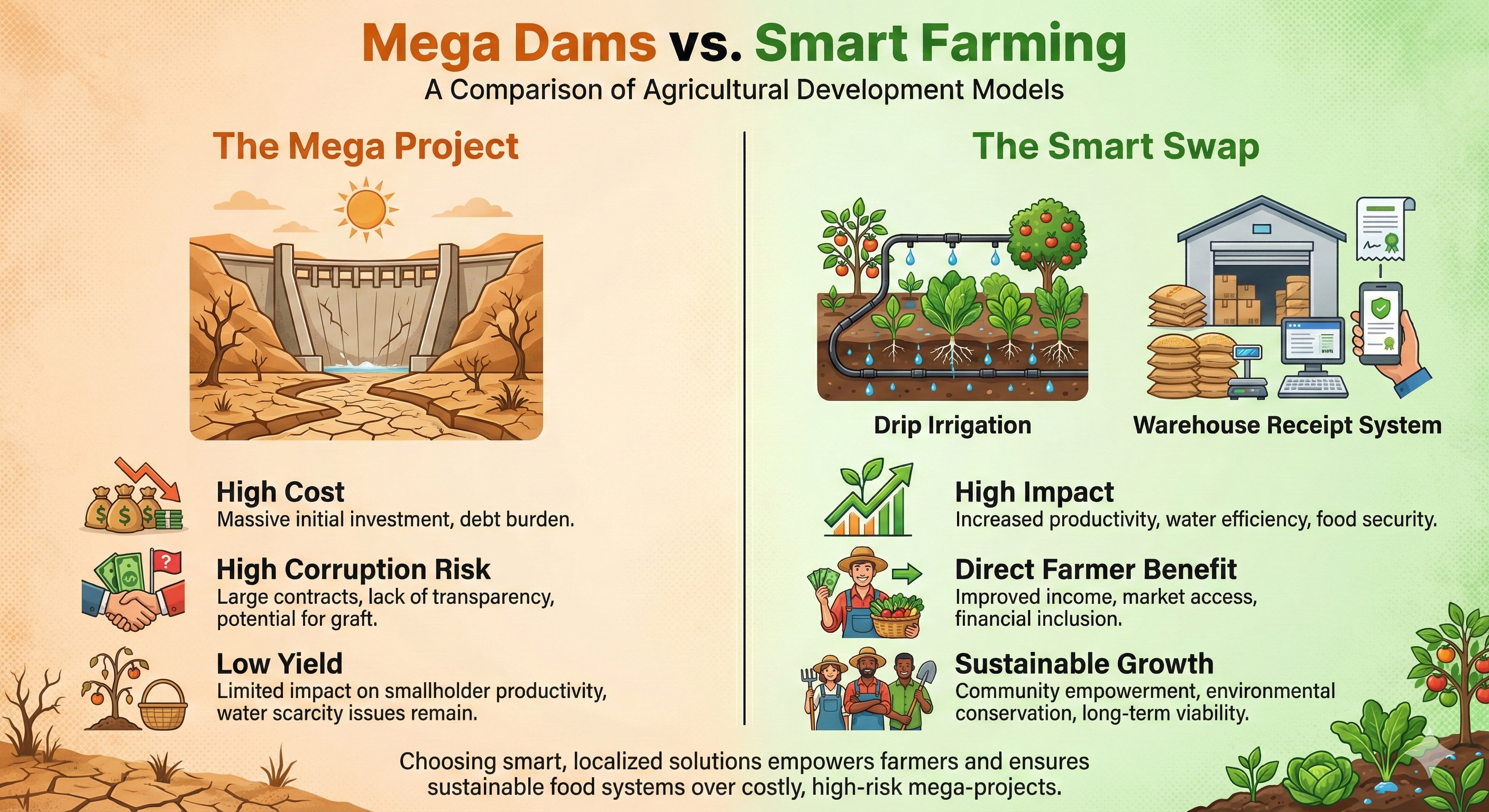

As the government targets 2 million acres for irrigation under the new debt swap initiative, the ghost of the Galana Kulalu project looms large. Just days ago, on January 26, 2026, the government announced plans for six new mega dams, signaling a return to the large-scale infrastructure strategy that failed so spectacularly in 2014. The original Galana Kulalu pilot consumed Sh7 billion to produce maize at costs higher than market price, collapsing under poor planning and corruption. Critics argue that repeating this “big dam” strategy ignores the hard-learned lessons of the past.

The disconnect is palpable. While the state plans mega-projects in arid lands, small-scale farmers—who produce the bulk of Kenya’s food—are struggling with basic input costs and lack of market access. The “savings” from the debt swap would likely yield higher returns if invested in decentralized solutions: household water pans, small-scale drip irrigation kits, and the Warehouse Receipt System (WRS) to help farmers store grain and avoid price exploitation by middlemen.

If the Sh129 billion is poured into another series of mega-dams, the funds risk being absorbed by contractors and consultants, leaving the country with more debt and no food. The success of this swap depends on shifting focus from concrete structures to the actual economics of farming—lowering production costs and ensuring profitability. Without this shift, we are merely “mixing oil and water” again, hoping that high-finance infrastructure will somehow trickle down to the grassroots.

References:

Capital Business Govt plans six mega dams, targets 2mn acres in irrigation push

The Star Government plans six mega dams, targets 2 million acres for irrigation push

🌦️ Wet West, Dry East: Why One Strategy Won’t Work for All in MAM 2026

The Kenya Meteorological Department (KMD) has dropped its forecast for the March-April-May (MAM) long rains, and it paints a picture of two very different planting seasons.

The Good News: If you are in the Highlands West of the Rift (Trans Nzoia, Uasin Gishu, Kericho) or the Lake Victoria Basin, get your tractors ready. The forecast predicts near-average to above-average rainfall. This is the green light for high-yield maize farming.

The Warning: For farmers in the Southeastern Lowlands (Kitui, Makueni), Northeastern, and the Coast, the forecast is tough. You are facing “near-average to below-average” rainfall, with a high chance of insignificant rains—meaning showers that wet the dust but don’t sustain a crop.

The Takeaway: Don’t copy your neighbor in Eldoret if you live in Machakos. The government is urging everyone to plant, but what you plant matters more than ever.

West: Go for maximum yield (600 series maize).

East/North: Go for survival (fast-maturing crops).

References:

Nairobi Leo Kenya Met Issues March-May 2026 Long Rains Forecast

Daily Nation End of drought in sight, but coming rains will be insignificant for arid regions

All Africa Above-Average Rains Expected in Key Regions, Weatherman Warns of Dry Spells Elsewhere

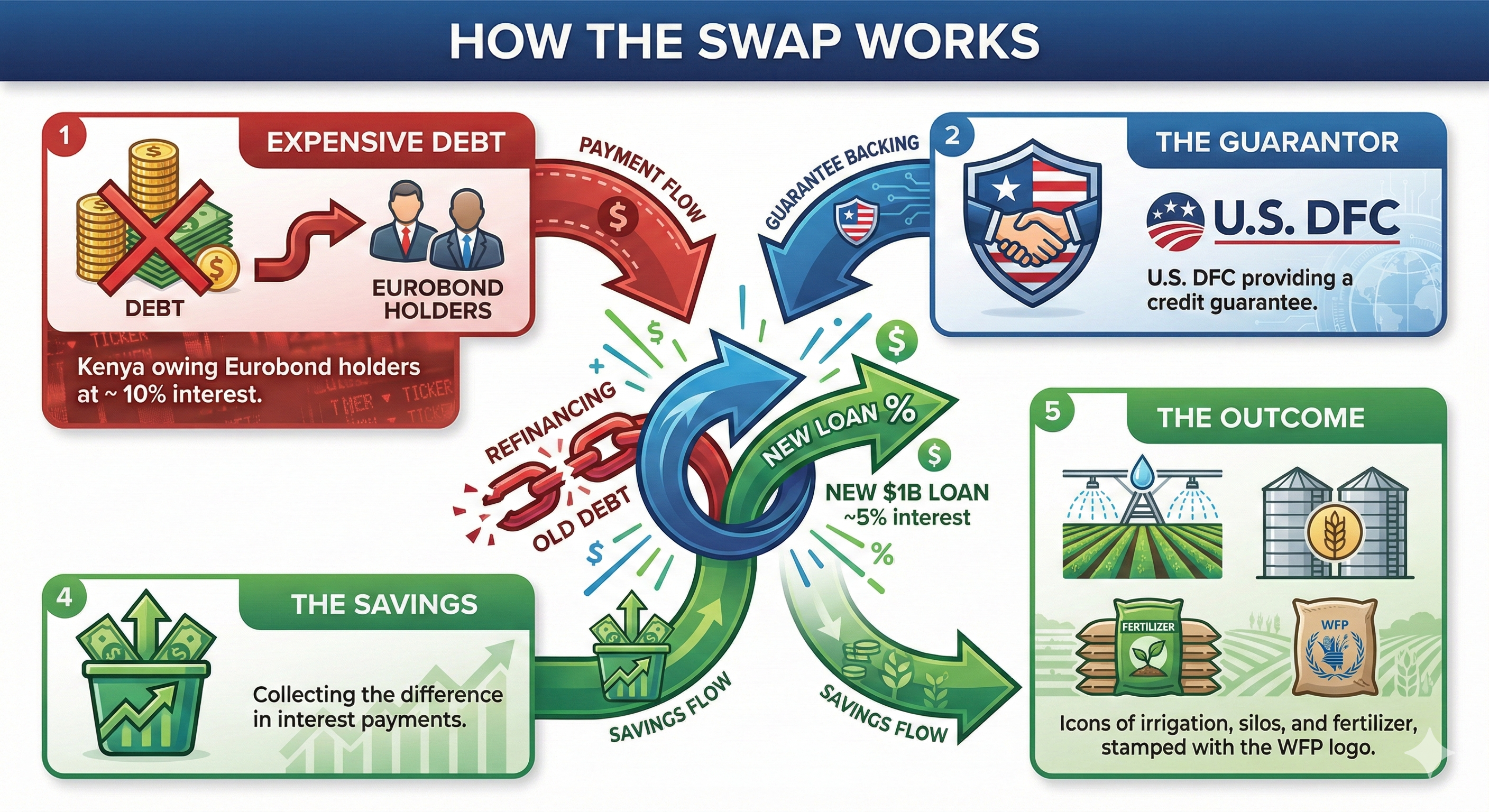

Kenya is on the verge of finalizing a landmark $1 billion (Sh129 billion) debt-for-food security swap, a sophisticated financial maneuver designed to rescue the country from a suffocating liquidity crunch. By leveraging a guarantee from the U.S. International Development Finance Corporation (DFC), the Treasury intends to refinance expensive Eurobond debt with cheaper, concessional loans. The plan is financially astute: it swaps high-interest commercial debt for lower-interest obligations, a move that prompted Moody’s to upgrade Kenya’s credit rating to B3 and stabilize the outlook on the nation’s sovereign debt.

However, the deal comes with a catch that transforms it from a simple refinancing operation into a complex development experiment. The interest “savings” generated from this swap must be ring-fenced and funneled directly into food security projects, managed in partnership with the World Food Programme (WFP). This arrangement effectively outsources a portion of national planning to an international body, admitting that the state needs external discipline to ensure funds aren’t diverted. While this stabilizes the shilling and pleases bondholders, it raises a fundamental question: is this a genuine strategy to feed the nation, or simply financial engineering to avoid default?

The stakes could not be higher. With 3.4 million Kenyans facing acute food insecurity and public debt service consuming over two-thirds of tax revenue, the government is betting that this “financial oil” can mix with the “water” of local agriculture without separating. If successful, it provides fiscal breathing room and lowers input costs for farmers; if it fails, Kenya will be left with the same debt burden and no improvement in the cost of living for the average wananchi.

When a private company’s neural nets began to unmask the hidden flows inside M-Pesa, the discovery jolted more than the fintech sector — it forced Kenya to confront a systemic question: who watches the watchers, and on what rules? The rollout of AI-driven compliance tools at Safaricom was never merely a tech upgrade; it arrived as part of a national emergency — a response to international pressure, spiralling fraud, and regulatory failure. The Financial Action Task Force’s increased-monitoring designation and months of global scrutiny had already pushed lawmakers and regulators into a sprint of reforms; industry actors answered with models that could learn patterns humans could not. But those same models required data — vast, granular, and often personal — and the legal scaffolding for such access was changing in real time. Kenya’s recent cyber-law overhaul and parliamentary amendments to the Computer Misuse and Cybercrime Act expanded state powers over online infrastructure, tightened penalties for SIM-swap and phishing offences, and gave the National Computer and Cybercrimes Coordination Committee sweeping directive authority over platforms and applications. Those moves addressed real harms — SIM swap fraud, phishing, and mass laundering — but they also recalibrated the balance between surveillance and rights.

Video Courtesy: The Kenyan Wall Street Youtube Channel

That recalibration is tested in the day-to-day rub of enforcement. Regulators and the ODPC have begun to draw lines: the Data Protection Commissioner’s recent ruling against a major betting operator for excessive data demands underscores the point that AML objectives cannot be a carte blanche for limitless intrusion. In the Betika case the ODPC found the company’s demand for three months of a user’s M-Pesa statements at account-closure to be disproportionate and ordered compensation, signalling that data-minimisation and privacy remain legally enforceable even amid AML pressures. At the same time, FATF’s 2025 monitoring guidance — and independent analysis from ISS Africa — make plain that Kenya must also show measurable results in prosecutions, beneficial-ownership transparency, and risk-based supervision of non-financial entities (including gambling and virtual assets) if it is to repair global confidence. The practical implication is blunt: Kenya cannot satisfy international partners by papering laws alone; enforcement and proportionate procedural safeguards must accompany technical surveillance. Otherwise the country risks swapping one reputational problem (grey-listing) for another — a domestic legitimacy crisis born of heavy-handed data practices.

So where does Kenya go from here? The answer lies in design choices — legal, technical, and institutional — that make accountability a feature, not an afterthought. We recommend three urgent, interlocking reforms that turn the AI question into a governance opportunity: (1) Purpose-bound, time-limited data access. AML or security queries should be scoped narrowly and logged; full transaction histories must not be a default feed into private models. (2) Explainability + redress. Any automated decision that materially affects a person (account freezes, cash-outs blocked, KYC escalations) must carry a succinct, non-technical rationale and a fast appeals channel routed through an independent body. (3) Joint independent oversight. Operationalize a statutory ODPC–FRC technical review board with public reporting obligations, the power to audit both models and data requests, and a mandate to publish redaction and retention metrics. These are not frictionless reforms — they will slow some processes and impose costs — but that trade-off is precisely the point: legitimacy costs less than lost trust. If Kenya stitches these protections into law and practice — and couples them with meaningful prosecution of financial crimes and improved beneficial-ownership registers — it can convert the awkward moment of global scrutiny into a first-mover advantage: an African model of rights-based, explainable AI governance for financial systems. The choices made now will decide whether Kenya’s algorithms become instruments of accountability or mechanisms that hollow out public trust.

References:

Business Daily Security or surveillance? How amended cyber law could reshape Kenya’s online space

Daily Nation How AI can close trust gaps in Africa’s financial systems

The Kenyan Wall Street How Safaricom is Leveraging AI to Bolster M-Pesa Security and Efficiency

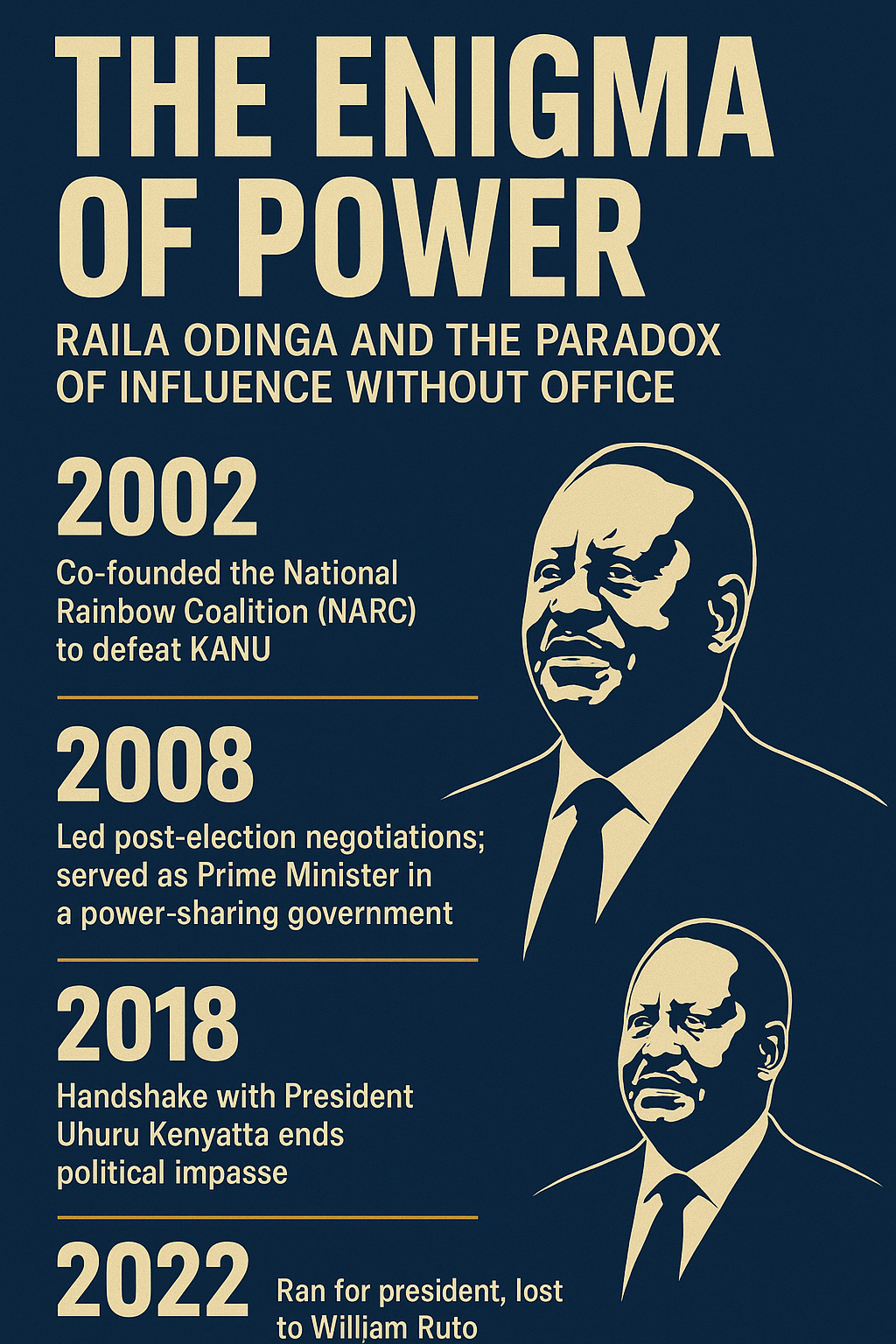

History rarely rewards those who come close — but in Raila Odinga’s case, proximity itself became the point of power. For more than four decades, Raila lived at the edge of power yet shaped every regime from within the shadows of opposition. He was, as The Africa Report aptly put it, “the man who lost every election but won Kenya’s democracy.” From the twilight of Daniel arap Moi’s rule to the dawn of Kenya’s multiparty renaissance, Raila’s defiance never waned — earning him both fear and reverence in equal measure. In 2002, when KANU’s dominance finally cracked, it was his dramatic declaration of “Kibaki Tosha” that propelled Mwai Kibaki to State House and ushered in the first peaceful transfer of power in Kenya’s history. Yet even in victory, Raila remained the outsider: betrayed by broken coalition promises, sidelined by those he helped elect. Still, he never relinquished the moral authority of the people’s voice. In 2005, his “Orange” movement defeated Kibaki’s draft constitution — a rare case of an opposition leader reshaping national destiny without holding office. And when the 2007 elections collapsed into violence, it was again Raila’s resilience that forced Kenya back from the brink, transforming a disputed vote into a dialogue for survival. Through pain, loss, and endurance, he became less a politician and more a barometer of Kenya’s democratic conscience — the man who could lose and still lead.

Raila’s power was never institutional; it was cultural, narrative, and profoundly human. He understood Kenya’s pulse — and weaponised symbolism like few before him. His aliases — Agwambo, Tinga, Baba — transcended politics, morphing into collective identities of resistance, belonging, and hope. His supporters saw in him their own unfulfilled promise; his rivals, a reminder that legitimacy cannot be decreed. Each administration that followed — from Kibaki to Kenyatta to Ruto — has been shaped, challenged, or legitimised by Raila’s political presence. As Prime Minister in the 2008 Grand Coalition, he co-supervised the nation’s reconstruction after post-election chaos and championed reforms that birthed the 2010 Constitution — arguably his greatest institutional legacy. That charter redefined Kenyan governance, devolving power to the counties and embedding civil rights into law, echoing the principles for which he had once been jailed. Later, his controversial 2018 “Handshake” with President Uhuru Kenyatta ended months of unrest following the disputed 2017 polls and restored political calm — though it also fractured his traditional support base. Yet, even that act reinforced his lifelong philosophy: that peace, not position, defines statesmanship. His later appointment as the African Union’s High Representative for Infrastructure confirmed his continental stature — a statesman recognised beyond Kenya’s borders for blending political endurance with technocratic vision.

In the end, Raila Odinga’s paradox was not that he failed to capture the presidency, but that he redefined what power itself means in a fragile democracy. His defeats never diminished his influence; they amplified it. Every president who took office did so under the long shadow of his moral authority. He forced institutions to evolve, compelled courts to assert independence, and transformed the vocabulary of opposition into the grammar of governance. In his twilight years, even adversaries acknowledged that Kenya’s political story could not be told without him — that every victory or reform bore his fingerprints somewhere beneath the surface. He was both architect and agitator, healer and heretic, rebel and reformer. Raila Odinga never occupied State House, but he changed what it stood for — from a fortress of fear to a house answerable to its citizens. And as the nation continues to wrestle with the legacy of leadership and legitimacy, his life offers a sobering truth: that true power is not seized, but earned — and sometimes, it lives longest in the hands of those who never hold the crown.

References:

The Africa Report Raila Odinga: The man who lost every election but won Kenya’s democracy

The Star Raila Odinga: The man who changed Kenya without ever ruling it

The Star Most consequential politician in history of Kenya bows out

All Africa Kenya Mourns Raila Odinga ‘The President’ It Never Had

TRT World Raila Odinga: Kenya’s political enigma never left the stage